|

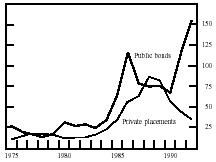

Information > Manual 166 > This page THE ECONOMICS OF THE PRIVATE MARKET Part 1: An Economic Analysis of the Traditional Market for Privately Placed Debt Overview of the Traditional Private Placement Market Part 1 of this study describes and analyzes what is now called the traditional market for privately placed debt. Until the development of the Rule 144A market in 1990, it was the entire market for private debt. It continues to be the larger of the two markets. Unless otherwise noted, in part 1 the terms private placement and private debt refer only to debt securities issued in the traditional market, and the term private market refers only to the traditional market for privately placed debt. 4 Taken as a whole, the traditional and the 144A private placement markets are a significant source of funds for U.S. corporations. Their importance can be seen by comparing gross offerings by nonfinancial corporations of private and public bonds (chart 1). Between 1986 and 1992, for example, gross annual issuance of private placements by such corporations averaged $61 billion per year, or more than 60 percent of average issuance in the public market (table 1).5 In 1988 and 1989, private issuance actually exceeded public issuance, as the financing of acquisitions and employee stock ownership plans boosted private offerings. However, public issuance surged in 1991-92, partly because of the refinancing of outstanding debt, and private issuance fell. The punitive prepayment penalties normally attached to privately placed debt make refinancing unattractive to issuers even when interest rates are falling. A similar comparison of private placements with bank loans, another major source of corporate financing, is difficult because of a lack of data on the gross volume of new bank loans and because of differences in maturity. Comparing outstanding bank loans with estimates of outstanding private placements is possible, however. At the end of 1992, bank loans to U.S. nonfinancial corporations were $519 billion, whereas outstanding private placements of nonfinancial corporations were approximately $300 billion, or somewhat more than half of bank loans. At the same time, outstandings of public bonds issued by nonfinancial

Sources: Federal Reserve Board and IDD Information Services.

Source. Federal Reserve Board and IDD Information Services. corporations stood at $775 billion. 6 In short, the private placement market has provided a substantial fraction of corporate finance in the United States. Most private placements are fixed-rate, intermediate- to long-term securities and are issued in amounts between $10 million and $100 million. Borrowers vary greatly in their characteristics, but most are corporations falling into one of three groups: mid-sized firms wishing to borrow for a long term and at a fixed rate, large corporations wishing to issue securities with complex or nonstandard features, and firms wishing to issue quickly or with minimal disclosure. Investors are almost always financial institutions. Life insurance companies buy the great majority of private placements of debt.

Principal Themes of Part 1 and Key Definitions Click

here to download The Economics of the Private Market in .pdf format |